Find out what’s happening to Social Security payments and how it will affect retirees in the near future

Recently, the Federal Reserve has sounded the alarm regarding Social Security payments, as they could change as we know them. Retirees in particular may receive disappointing news as the new cost-of-living adjustment (COLA) announcement was confirmed. The Federal Reserve has issued a warning that these essential benefits could be further cut in the future years, leaving pensioners to cope with smaller gains in Social Security income. The era of large increases in Social Security benefits may be ending now that inflation is under control. According to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), the Social Security Administration (SSA) calculates COLA.

What you need to know about the Federal Reserve warning and the future of Social Security payments

The adjustments are intended to help Social Security benefits stay up with inflation, preserving pensioners’ purchasing power over time. Due to high inflation levels and the economic instability caused by the pandemic, retirees have seen an 18.8% increase in their benefits over the past three years. Nonetheless, the success of the Federal Reserve in controlling inflation might signal the end of significant COLA increases. As a result, Social Security recipients should anticipate fewer changes in the years to come as inflation declines.

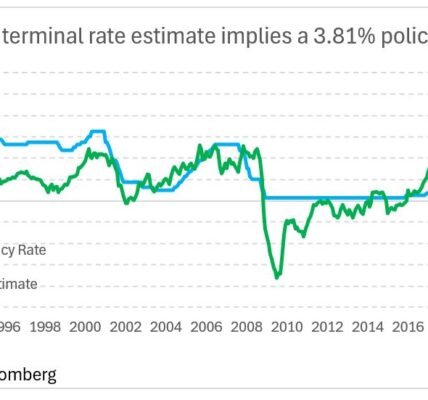

The Federal Reserve lowered the Federal Funds rate by 50 basis points to a range of 4.75% to 5% in September 2024, marking the first rate cut in four years. This move demonstrates the central bank’s confidence that inflation is currently under control. The economy as a whole benefits from the Fed’s efforts to keep inflation under control, but Social Security-reliant pensioners may be let down. As a result, when inflation slows, the SSA may not need to increase payments as much, making it harder for retirees to keep up with rising living costs.

However, if the downward inflation trend continues, the final COLA for 2025 in September may not exceed 2.6%. The drop in energy prices, particularly those of oil, which has fallen below $70 a barrel, the lowest level in almost a year, is one of the primary causes of this trend. The possibility of a higher COLA is further diminished by the fact that declining energy prices, which play a significant role in the overall rate of inflation, suggest that annual inflation will continue to decline. Moreover, the Federal Reserve has said that inflation will likely continue to decline in the future, with its long-term target set at 2%.

Inflation is predicted to be at 2.3% by the end of 2024 and to have decreased to 2.1% by the end of 2025. This means that instead of the 2.6% COLA expected in 2025, the COLA in 2026 could be as low as 2.2%. Retirees will have to save aside money for these minor COLA adjustments. The statistics are retroactive, based on historical economic data, and may not accurately reflect the financial challenges that pensioners are currently facing, such as rising costs for necessities like food and electricity, even though the COLA increases are meant to help retirees keep up with inflation.

Will lower interest rates eventually benefit retirees?

One possible advantage, despite the overwhelming prospect of lesser Social Security check increases, is that cheaper borrowing costs may arise from the Federal Reserve’s interest rate reductions. For retirees who have debt from mortgages or auto loans, lower interest rates may provide financial comfort. Increased financial flexibility for retirees could result from lower borrowing costs offsetting the reduced COLA adjustments.

Furthermore, even though the COLA is largely a reactionary adjustment based on historical inflation, the overall decline in inflation may help stabilize seniors’ expenditures. Lower inflation could prevent retirees from experiencing the dramatic increase in living expenditures that they have in recent years.