From 65 Cents to $5.69: Big Macs Show How The Federal Reserve Ate Your Bills’ Buying Power

Few companies are more effective at cutting costs and increasing production than McDonald’s, with its “billions and billions served,” in more than 100 countries. That ubiquity and consistency prompted The Economist to introduce the Big Mac index, which attempts to measure purchasing power parity by averaging the cost of a roughly comparable good across both time and geography.

When the index was introduced in 1986, the average cost of a Big Mac — according to the classic jingle, “two all-beef patties, special sauce, lettuce, cheese, pickles, onions on a sesame seed bun” — was around $1.60.

The 1974 commercial that turned the recipe into poetry (and offered prizes to those who could recite the slogan in under three seconds) concluded with the line “where your dollar gets a break every day.”

When the jingle debuted, the cost was around 65 cents. You could pay for it with a single dollar bill and expect change. Today that price has risen $5.69. The purchasing power of your dollar, according to burgernomics, has fallen 90 percent in the past 50 years (the Federal Reserve Bank of St. Louis puts that number at 85.3 percent, and it’s reasonable to believe ingredients, labor, and real estate inflation prompted McDonald’s to charge 10 percent more between $1.60 and $4.69).

Fifty years ago you could buy, with the five-ish physical dollar bills it takes to buy one Big Mac today, depending on which stats you use, between six and nine more Big Macs.

(If you’re outraged about inflation, good, you’re ahead of the game. But hang in there. Today we want to frame the question in physical currency.)

If buying a Big Mac in one-dollar bills requires approximately six times as many one-dollar bills as it did in 1974, why is the government still printing billions of one-dollar bills?

Inflation reduces the purchasing power of physical currency. Six physical dollar bills are required to buy a Big Mac, compared to one in 1974 and two in 1986. (In each case, by chance, you’ll receive four dimes in return — what you do with those will matter later.)

Thanks to inflation — rampant money-printing — by the Federal Reserve, each purchase of a Big Mac or anything else must include more physical banknotes, increasing the costs of storing, transporting, and handling money.

In low-inflation countries, paper currency denominations rarely change. The European Central Bank, Bank of Japan, Bank of England and the Bank of Canada have all redesigned their currencies with different monarchs and motifs, and added security features, but have neither changed the face value nor issued higher-denomination bills.

By contrast, in high-inflation countries, denominations of currency issued eventually adjust, but often lag behind rapid devaluation. The 100 trillion Zimbabwean dollar bill is only one of the largest denominations ever in circulation, and was worth just ten American dollars, in Zimbabwe, in 2009. One USD or 100,000,000,000 ZD.

As of March 2024, 80 percent of all transactions in Zimbabwe were in US dollars. The market has spoken.

Why don’t central banks adjust denominations more frequently to maintain stable purchasing power? Like everyone else, central bankers face trade-offs with every decision.

Even central banks have some incentive to keep their currency attractive to users. Currencies backed by governments enjoy mandatory legal-tender status, meaning people and businesses have to accept them — sort of. The monopoly on issuing currency does not protect central bankers from stiff competition. If cash becomes too difficult to carry or store, especially in large quantities, people convert to substitutes.

In particular, users value certain key features in modern currencies:

- Portability: Large purchasing power contained in a lightweight textile (paper money isn’t paper) allow us to carry around significant sums (and even put them through the wash occasionally) as stable, negotiable representations of value.

- Divisibility: Small denomination bills allow us to engage in small transactions, and to make change for larger bills.

From the search for balance emerges the notion of an optimal denomination of money, the one that minimizes the number of denominations, and the amounts of bills to be exchanged, while increasing the probability of receiving exact change.

If maximizing use by the public is the key indicator of a successful currency, central bankers who serve as monetary authorities should provide bank notes to meet public demand. Widespread ease of use of the legal tender currency benefits central bankers.

So why don’t central banks adjust the denomination of bills more often, to match their purchasing power? India recently issued a new denomination. What incentives do central bankers have to keep currency denominations small, when inflation makes cash increasingly meaningless and inconvenient?

1. Denying the Reality of Inflation.

Introducing a new bill of higher denomination into circulation would constitute a clear message by the monetary authority that inflation is real. Controlling how people feel about the value of money, and how we adjust our behavior in response to our perceptions and expectations, is a core function of a central bank. If people properly perceive the threat to their own security posed by continual inflation and overspending, they might turn against government interests. The most precious single asset a central bank can possess is credibility.

2. (More) Profiting from the Printing of (More) Physical Bills

Not adjusting higher-denomination bills for real purchasing power increases the number of banknotes and coins minted, raising the cost of printing money. As inflation rises and each note buys less, more physical money is needed and these costs accelerate.

Central banks make money through seigniorage — government profit from money creation — when the face value of currency produced exceeds production costs. Printing more money increases expenses and leads to larger contracts for production, often but not always staffed to private firms. Where institutions and oversight are weak, printing more money increases opportunities for bureaucrats to profit.

If you need six bills to buy your Big Mac, the cost of printing (and the potential for graft) is six times higher. Argentina experienced such rapid inflation that even doubling the face value of its existing currency in circulation, their highest bill as of December 2024 is worth only 20 USD. The extra cost of printing more currency, as of 2022, totalled at least $93 million each year. The decision to continue printing lower denominations in higher volumes even led a former vice president to illegally buy Argentina’s largest private mint, a crime for which he was later convicted. On a smaller scale, lobbying to keep the near-worthless penny in circulation is led by the firms who make ‘coin blanks’ from zinc for the mint.

3) Devaluing Small Change, and Passing the Cost On.

More currency in circulation and more physical transactions create an industry that benefits from maintaining the status quo. There is more incentive to install and maintain ATMS, which must be filled with cash more often, given their limited physical capability. That means more armored trucks, and truck drivers, are needed.

As inflation rises, small change denominations slowly become irrelevant. Discount markets emerge to suck up our low-value change. The Salvation Army has capitalized on that habit we’ve built of treating small change as disposable, as has CoinStar. Your Big Mac may be “rounded up [to the next dollar] for Ronald McDonald House,” starting in 2019.

In 1974, you’d pay for a Big Mac and get (about) four dimes in change. Those four dimes could buy fries and a soft drink, or ice cream in 1974. The comparable upgrade between just a burger and a Big Mac meal in 2024 is $2, for a larger portion (of less-pricey, probably less-healthy ingredients) in both soda and fries. You’d be inclined wait for your change and hang onto it, even if you didn’t take the extra food. Even now, McDonald’s wouldn’t ask you to round up two extra dollars. But what’s four dimes? What will you do with them, anyway? Small change becomes less meaningful.

We pay the small-change trouble tax ourselves, and take the sting out of inflation a little.

(It’s worth noting that these transaction costs to an inflated currency have much less effect on institutional players, including central banks, who deal mostly in non-physical currency substitutes.)

According to contemporary reports in the Review of African Political Economy, when Zimbabwe dollarized its economy in the late 2000s, after massive hyperinflation, it destroyed a thriving industry in currency dealing, storage, collection, and exchange.

4. Discouraging Unsanctioned and Private Market Transactions.

Carrying large amounts of cash is inconvenient. Making cash difficult to use in large quantities makes money laundering easier to detect and raises the potential costs of underground transactions. Increasing the operational cost of cash is weighed against the desire for privacy, and pushes more transactions into the legal (taxable) realm or into cash alternatives visible (taxable) to central bankers.

When high-denomination bills are issued, they immediately become the cheapest medium of exchange for people who don’t want their business known to the government. When in 1969 the Nixon administration discontinued the large denomination US dollar bills ($500, $1,000, $5,000, and $10,000 were last issued in 1969 and haven’t been printed since 1941) one argument was that it was an effort to combat organized crime. More recently, the European Central Bank discontinued its high value notes, citing similar logic.

5. Pressure Toward Digital Alternatives

A fifth possibility for central banks not adjusting the face value of currency to keep up with inflation is somewhat counterintuitive. Despite central banks’ incentives to maintain lucrative seigniorage and exclusive currency status, central banks may want to push people away from all-cash transactions, as we saw with high-denomination bills, money laundering, and organized crime. Making cash transactions inconvenient (because they are less portable and less divisible, and you lose marginal value to couch cushions, and we all lose time to sorting, exchanging, and counting cash) will benefit a central bank that sees reason to accustom citizens to digital transactions. At some point (public choice theory would suggest) the value of tracking (and taxing) all currency will exceed the sum extracted from the public through seigniorage and the monopoly on fiat currency (there are more alternative currencies online). Beware a central bank digital currency, for this and many other reasons eloquently enumerated elsewhere.

Will We See a $500 Bill (Again)?

Most of us don’t consider the possibility of supersizing US currency denominations. We’ve grown so accustomed to our fives, tens, and twenties, that we fail to recognize what it really means that a not-so-great-for-you burger that cost 65 cents in 1974, and $1.60 in 1980, costs $5.69 today. The one-dollar bill you found in your college sweatshirt is still spendable, but it only buys a quarter of a burger. The quarter in your grandmother’s couch could buy a McDonald’s coffee when she dropped it in there. Now 25 cents won’t buy a single thing on the menu, except a sauce packet or paper bag in some locations.

Inflation isn’t (just) prices going up.

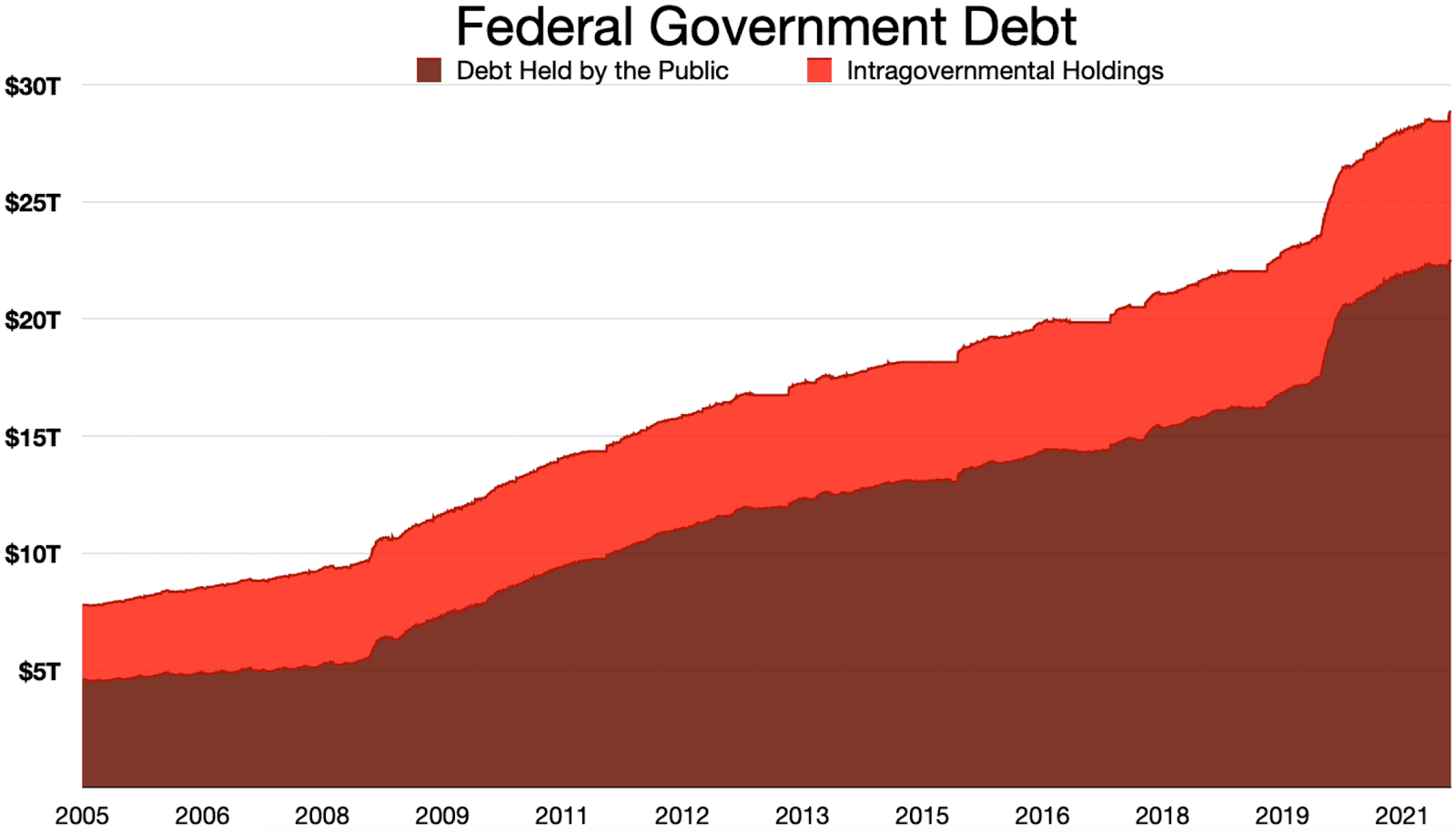

Your physical currency is losing 2 percent of its value per year. The Fed’s target(!) inflation rate has gobbled up 85 percent of the Big Macs you could have bought. Your other six and a half burgers got eaten by the Federal Reserve, courtesy of government spending.

Read More

The Real Reason Fast Food Is So Expensive

The Federal Debt Just Eclipsed $36 Trillion